Contact The Editor

Contact The Editor

Articles By This Author

Articles By This Author

To understand the economy, you've got to resort to psychology. Throughout the recovery, forecasters, including those at the Federal Reserve and the International Monetary Fund, have repeatedly overestimated the economy's strength. They've predicted faster economic growth than has occurred.

The main reason for the errors, I have argued, is that the forecasters have underestimated the influence of the financial crisis and Great Recession on people's confidence. Lower confidence reduced Americans' willingness to spend. My argument has applied to the United States. Some new figures now suggest that the same phenomenon operates globally.

The figures come from the Pew Research Center, which interviewed 45,435 adults in 40 countries about their economic outlook. Almost seven years after Lehman's collapse, attitudes remain remarkably downbeat. One question Pew asked is whether respondents rated the "current economic situation in their country very good, somewhat good, somewhat bad, or very bad." Majorities in 27 of the 40 countries answered bad, says Pew's Bruce Stokes. (These results combine the two gradations of good and bad.)

To be sure, there were regional differences. Respondents in the Asia-Pacific area, including China, judged their economies good by a 51 percent to 47 percent margin; in Africa, respondents were also almost evenly split, with 48 percent answering good and 51 percent saying bad. But elsewhere, verdicts were lopsided. In Europe, it was 70 percent bad to 28 percent good; in Latin America, the margin was 63 percent to 36 percent. The U.S. result was a little closer, 56 percent bad and 40 percent good.

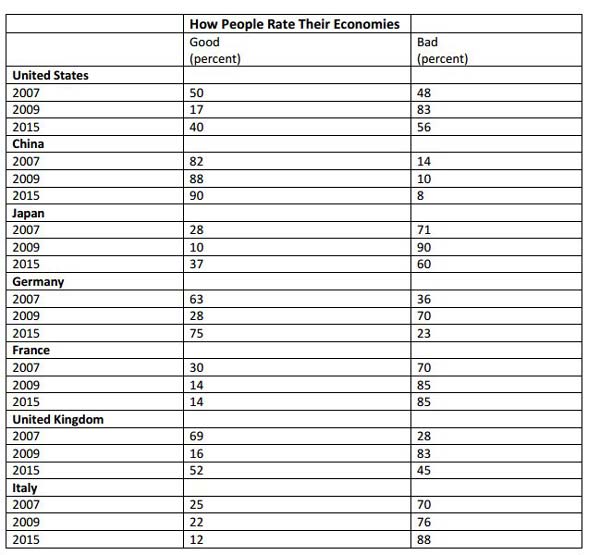

It's also true that more people are optimistic now than at the depths of the global recession in 2009. Then, only 17 percent of Americans rated the economy good, roughly half today's level; but that reading is still below the 50 percent registered in 2007 before the financial crisis. Only a few countries have confidence levels higher than before the crisis. Germany is one; 75 percent of Germans rate their economy good, up from 63 percent in 2007.

What we have is a global funk. It's a hangover from the financial crisis and Great Recession, not gloom so much as worry and restraint. Because the economic damage — lost jobs, lower profits, foreclosed mortgages, depressed trade — exceeded anything experienced since the Great Depression, people now prepare for the unknown more than before. In practice, they save more and spend less.

The shifting psychology confounds economic models, based (as most are) on earlier business cycles. Instead of a vigorous recovery, we get the opposite. Weaker consumer spending undermines business investment because companies can satisfy demand without expanding. Weaker investment then further retards the expansion. The Pew data convince me that this vicious circle, long at work in the United States, has its international counterpart.

Of course, countries' feeble confidence also reflects local circumstances. Only 13 percent of Brazilians rate their economy good; the causes surely include high inflation and a host of scandals that have rocked the country. By contrast, confidence in China remains high (90 percent rate the economy good), even though growth has recently slowed. One possible explanation is that the Chinese still give more weight to past experience.

The table below provides Pew's data for seven major economies for three periods: now; in 2009 during the recession; and in 2007 before the crisis.

Comment by clicking here.